Goldman Weighs In On Accelerated Copper Import Tariff Timeline

President Trump’s national security probe under Section 232 of the Trade Expansion Act of 1962, launched in February to review raw copper, refined copper, copper concentrates, copper alloys, scrap copper, and other copper derivatives imported into the U.S, directed the Commerce Department to deliver tariff recommendations to the White House within 270 days. That review process has likely been accelerated, as a new report suggests U.S. copper imports could be enacted in the near-term.

Sources told Bloomberg that the Trump administration is moving quickly with its review of copper import tariffs and will likely act well before the 270-day deadline, which was expected between September and November. The new timeline has now shifted to mid-May.

Commenting on the shortened timeline, Goldman’s Eoin Dinsmore, Aurelia Waltham, and others provided clients with a critical Q&A addressing physical market flows and pricing across various exchanges:

What is the impact on physical market flows?

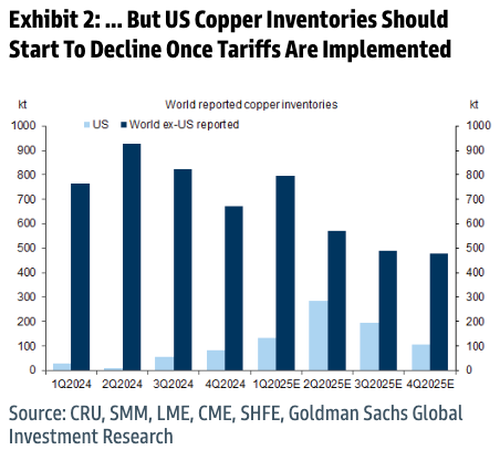

Greater certainty on copper tariffs means COMEX is likely to trade at a higher premium to LME, but there is less time to ship metal to the U.S. Assuming tariffs are implemented in May, we think shipments to the U.S. will likely be fast tracked, with net imports in April potentially jumping 200kt[1] above the standard 60-70kt/month, albeit with upside risk. However, with the possibility of earlier tariff implementation, we now expect U.S. stocks to decline by 30-40kt/month from mid-to-late Q2 onwards. Thus, we avoid a stock glut in the U.S. in Q3 2025, when we expect global copper market tightness to be most pronounced.

What is the impact on the LME price?

We see stranded stocks at the low-end of our range – a 200kt increase in U.S. stocks, and a possible 60kt loss of refined production from lower U.S. exports of copper concentrates and scrap. But by Q3, when we forecast the bulk of the 2025 annual global deficit will occur, U.S. stocks should have started to normalize. Thus, the expected H2 crunch should be less pronounced, which reduces upside risk to our LME price forecast. We hold to our 3/6/12 Month LME price forecasts of $9,600/t, $10,000/t and $10,700/t, and flag near-term downside risk from the trade policy update on April 2nd.

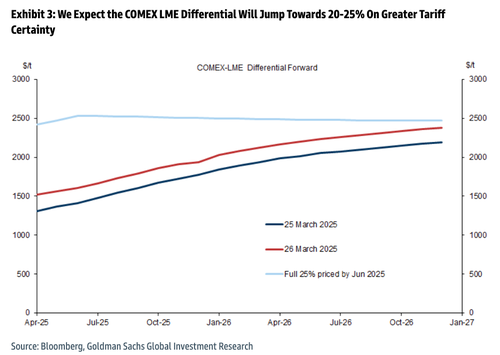

Will COMEX now price the full 25% tariff over the LME?

Factoring in uncertainty on the tariff level and high U.S. inventories, we think an implied tariff of 20% should be the cap in the near-term. This has also been a level regularly cited as a good exit point in numerous client meetings.

Will Sep-Dec 2025 spreads tighten?

We close the trade recommendation to go long Sep-Dec 2025 timespreads. Despite Q3 2025 being the key point for global copper market tightness, the spread will no longer need to rise to a level to halt exports to the U.S. Based on our Q3 ex-US reported inventories forecast, the likely backwardation would be only $0-60/t, close to current levels.

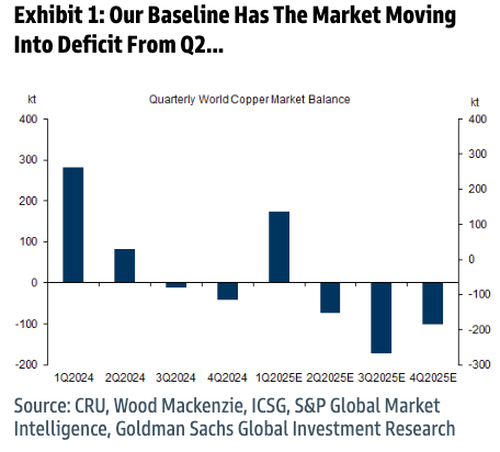

The analysts see global copper markets shifting into a deficit in 2Q25.

U.S. copper inventories should begin declining after tariffs are enacted.

Analysts expect the COMEX and LME spread to be capped soon.

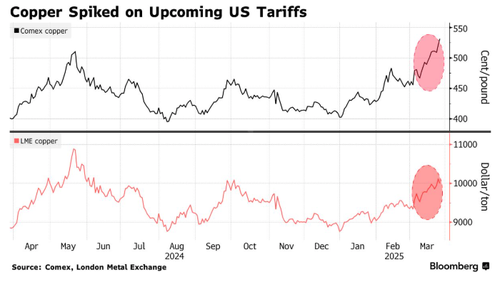

The Bloomberg report sent copper prices on Comex up 3% to a record $5.37 per pound. Meanwhile, the benchmark price on the London Metal Exchange fell 2% to $9,893 per ton, widening the gap between the two contracts to about $1,700 per ton

„The news today is this story of Copper tariffs coming sooner than possibly expected… LME/CMX arb at $1750-1800 in July (+$300 to start today) or 18% Tarrff expected,” Goldman analyst James McGeoch told clients earlier.

McGeoch offered some thoughts about today’s news and copper trading:

-

The durability of this move is significantly greater than 2024. Balances are tight, there is a fundamental driver and a technical ampifier (that technical is also fundamental in that the U.S. is short metal, fundamentally they want to change that).

-

As price traded back to $10k last night, the CMX premium now well above 15%, as it trades through record highs to 529 (+1.5%), traders (with vested interests) talk about price to $12k

-

Remember that whilst metal is being stacked in the U.S., we had last week the China SRB suggest it was also looking to build stocks of critical minerals: cobalt, copper, nickel, and lithium link. So Apparent demand (at either end, U.S. and China) is amplifying the effect of real demand (electrification, Chinese fiscal put, German infra plan), and tightening the balances further

-

Trading observation in discussion Monday – Positioning has not baked the above in. Regional contract differentiation leaves those with the global view on sideline (also too much idiosyncratic risk they lack edge to play). Point is the big rally lacks a big uptick in spec interest/positioning. The copper fwds have a lot to go, the incentives not in the curve and physical premiums doubled last week (first sign they are being impacted). The work now is dissecting physical location premiums and how the moves in inventory can impact near term demand. As we rally to $10k we may see some producing selling and as such spreads can remain bid.

-

CTA’s are as long as I can recall, the GS model suggests close to $18bn (historical max 19.6bn). This is where all the length is. CFTC weekly data showed a fairly meh inc for managed money accts (CME +9 to 22k lots, LME +2 to 63k)

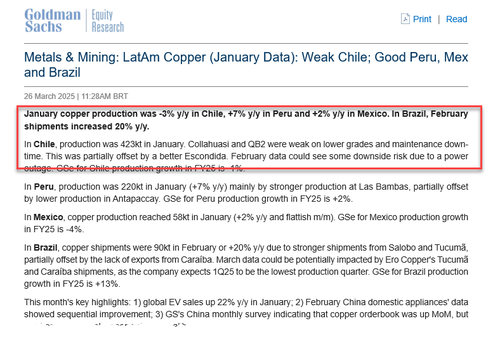

And we ask: What happens to global copper production with prices at record highs?

Now that tariffs are likely to be imposed sooner, importers will have significantly less time to rush copper shipments into the U.S.

Tyler Durden

Thu, 03/27/2025 – 06:55