Just A Correction, Or Is The Bull marketplace Over?

Authorized by Lance Roberts via RealInvestmentAdvice.com,

Is this just a correction after a strong bullish advance from November, or is the bull marketplace ending? If you read any of the headlines, you would propose the later. As noted by MarketWatch Last week:

“For the first time since early November 2023, little than 30% of S&P 500 stocks are trading above their 50-day moving event — a clear indicator of the current mediocre market’s breadth. This crucial drop from the 85% observed in summertime March and 92% at the beginning of January highlights a dramatic reverse in marketplace dynamics.

The 50-day moving average is frequently seen as a barometer for the short-term wellness of stocks. Falling below this level en masse suggestions that a broad swath of the marketplace is facing downward pressure. This shift comes amid escalating geopolitical tensions in the mediate East and renewed deals over inflation, which have collectively bored traders towards a more guarded standing in April.”

Of course, there are many “reasons” later for the drop in stock prices. Geopolitical stress between Israel and Iran and hotter-than-exected inflation date that paused Fed rate cuts throught sellers into the market. However, no of this is shaking, as we previously noted in “Blackout Of Buybacks:”

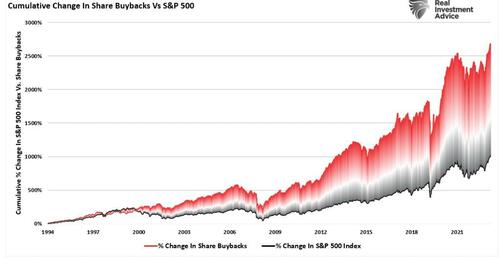

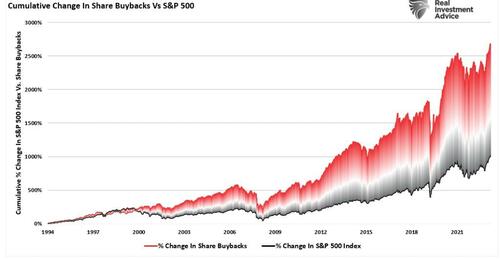

“Notably, since 2009, and accelerating starting in 2012, the percent change in buybacks has far outstripped the increase in asset prices. As we will discretion, it is more than just a casual correction, and the upcoming blackout window may be more critical to the rally than many think.” – March 19, 2024

Furthermore, the “blackout” of corporate buybacks coincided with an aggressively bullish investor sentiment. As we noted in that same article:

“Investor sentiment is one more time very bullish. Historically, erstwhile retail investor sentiment is excellently bullish combined with low flexibility, specified has mostly correlated to short-term marketplace peaks.”

We will return to this illustration momentarily, but given that corporate share buybacks have accounted for more than 100% of net equity purchases over the last 2 days, the blackout period combined with aggressive bullish sentiment was the recipe for a decline in asset prices.

Here is the math of net flows if you don't believe the chart:

Pensions and common Funds = (-$2.7 Trillion)

Households and abroad Investors = +$2.4 Trillion

Sub full = (-$0.3 T)

Corporations (Buybacks) = $5.5T

Net full = $5.2 Trillion = Or 100% of all equity purchased

Such is cruel to realize as we head into the remainder of the year. It will find whother this is just a correction within a bullish trend or something more significant.

Buyers Live Lower

In “No Cash On The Sidelines,” we discuss the import of knowing that “market prices” are set by the request and supply between buyers and sellers. It's wit:

“As noted above, the stock marketplace is always a function of buyers and sellers, each negotiating to make a transaction. While there is a Buyer for all seller, the question is always at “what price?”

In the current bull market, fewer people are going to sell, so buyers must keep bidding up prices to attract a seller to make a transaction. As long as this claims the case and exuberance increases logic, buyers will proceed to pay higher prices to get into the positions they want to own.

Such is the very definition of the “greater foot” theory.

However, at any point, for whatever reason, this dynamic will change. Buyers will become more Scarce as they refuse to pay a higher price. erstwhile sellers realize the change, they will rush to sale to a dimishing pool of buyers. Eventually, sellers will begin to “panic sell” as buyers evaporate and prices plunge.”

In another words, “Sellers live higher. Buyers live lower.“

We can see where the buyers and sellers “live” in the following chart, which shows where the highest volume occured.

This current correction is becoming creatively superior (bottom panel), which suggestions a bounce is likely toward the erstwhile support of the 50-DMA. For comparison, we can look at last year’s marketplace correction. As noted, the bullish rally into July peaked summertime that month. As the marketplace corrected, it bounced from overold conditions, allowing investors to reduce hazard and hedge portfolios. The markets will likely present investors with that chance soon.

Then, like today, many investors began to believe it was’t just a correction but something much more. However, the reality was that the “Buyers lived lower.’ Buyers stepped in as prices recommended the October lows, connecting with the return of corporate share buybacks.

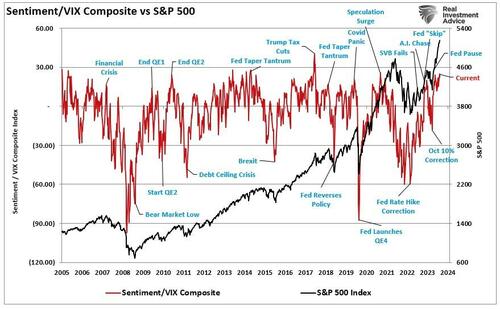

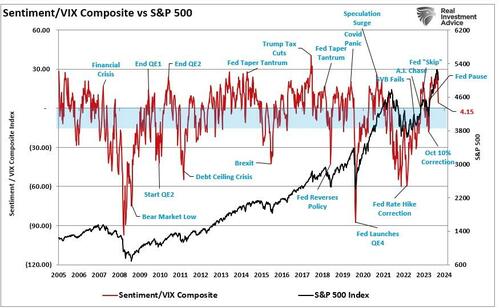

Sentiment Is Reversing Quickly

As I said, we request to revisit the sentiment illustration above. Investors’ more frothy, bullish sentiment is reversing rapidly on many fronts. The illustration below, the same as above, is the composite net bullish sentiment index of retail and professional investors distributed by the flexibility index (VIX). If this is just a marketplace correction, the index trends to bottom between zero (0) and negative (20). With a current reading of 4.15, down from 25.99 just 2 weeks ago, bullish sentiment has signedfully reversed.

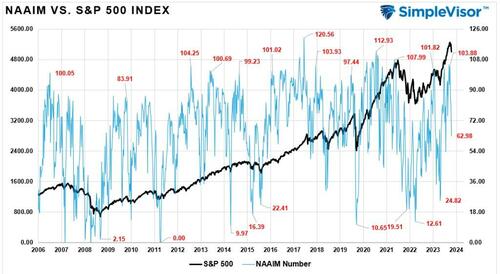

Notably, professional investor allocations to equities late observed at 103.88%, which has collapsed in just 2 weeks to just 62.98% exposition. (Professional investors are notorious for buying marketplace peaks.)

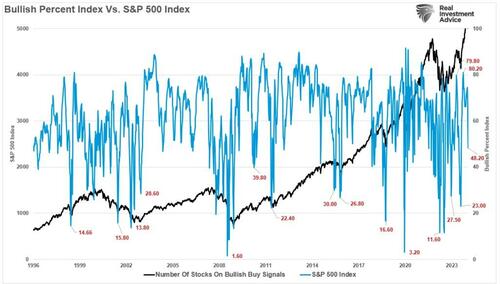

Also, the number of stocks on bullish “buy signals” has dropped from 80.2 to 48.2.

Furthermore, the number of stocks trading above the 50-DMA has fallen from over 80% to 37%, with money flow hitting levels lower than erstwhile marketplace bottom lows. Notably, with just a 5.5% correction from the last highest (as of last Friday), much of the work of cleaning the erstwhile overbought conditions is completed.

Given the crucial reverse in sentiment and short-term oversold conditions, we highly propose the markets will supply a reflective rally soon. However, with the number of bullish investors who got “Trapped” in the selloff, any rallies will likely be met with another selling.

However, despite the current “Panic’ in the media headslines, this is likely just a correction within an ongoing bullish market. specified is partially the case given that corporate share buybacks will resume in May, providing critical support for the markets heading into summer.

With that said, this correction, erstwhile complete, likely won’t be the last we see this year. marketplace past suggestions in could see another “Bumpy ride” heading into what many effects will be a certain contentious selection.

But that is an article we will compose erstwhile we get there.

Tyler Durden

Tue, 04/23/2024 – 13:05